The Advantages of Smaller Mortgage Lenders:

Why Choosing a Small Lender Can Be a Smart Move

In the complex world of mortgage lending, borrowers often face a choice between large national banks and smaller, and specialized mortgage companies.

Here is a list of all the banks in Australia

While we all know the big 4 banks, like ANZ, Commonwealth Bank, Westpac, NAB, etc.

It might seem like the obvious choice due to their scale and extensive resources, but smaller lenders offer distinct advantages that can make them a compelling option for many homebuyers.

Let’s explore the benefits of choosing smaller mortgage lenders and how they can provide a more personalized, flexible, and cost-effective mortgage experience.

The difference between banks and non-banks explained:

Banks

$ Are authorized deposit-taking institutions (ADIs) and can use

their funds to provide home loans.

$ They provide integrated banking packages including savings,

transaction accounts, and credit cards.

$ Networks of branches provide additional service but contribute

significantly to overhead costs.

$ The ‘Big 4’ banks are generally perceived poorly by the public and

have low customer service ratings compared to their competitors.

Second-tier banks

$ There are a surprising number of household names beyond the

‘Big 4’ including ING Direct, Macquarie Bank, Suncorp, St

George, Bank of Queensland, BankWest, Adelaide Bank, Citibank

and AMP.

$ While some are now owned by the big banks it is worth

considering their competitive offerings.

Building societies and credit unions

$ These non-profit cooperatives are owned by the people who use

their services.

Each member is both a customer and a shareholder.

$Interest Rates can be very competitive.

$ Member deposits are used to fund loans.

$ Like banks, they offer a wide variety of banking facilities with a

focus on customer service.

$ They are regulated in the same way as banks.

Here is a list of all second-tier lenders

Non-bank lenders

$ They do not hold an Australian banking license so cannot accept

deposits. They therefore source wholesale funding via investors,

financiers, trusts and even the ‘Big 4’ banks.

$ Mortgage Managers are part of this group but rather than sourcing

wholesale funds, they arrange finance for individual loans, lend it

out under their own brand and perform a customer service role

for the term of the loan on behalf of the underlying lender.

$ They do not have the overheads of an extensive branch or ATM

network.

$ The appeal for customers has been lower interest rates, and more

flexible lending criteria (e.g. for low doc or non-confirming loans)

and higher loan-to-valuation ratios (LVRs).

$ An emphasis on customer service, faster loan processing times,

and responsiveness are other selling points compared to the big

banks.

$ Lower rates are however often balanced by higher fees.

$ Clients are sometimes concerned about the financial security of

these lenders, particularly with the potential of another global

credit squeeze.

Non-bank lenders may be less able to access funds, so that they are

more likely to pass on higher costs via interest rate

rises.

$ They tend to have limited products and services so you might not

be able to use them for all your financial needs.

One of my biggest frustrations is seeing borrowers regularly make the

mistake of choosing a more expensive loan with a better-known lender.

NON-Bank Lenders List

Benefits of Smaller Mortgage Lenders

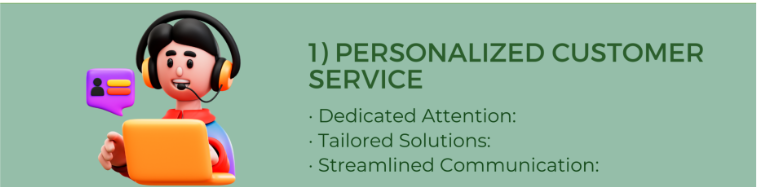

1. Personalized Customer Service

One of the most significant advantages of working with a smaller mortgage lender is the level of personalized service you receive.

Smaller companies typically have fewer clients compared to large banks, which allows them to offer a more individualized experience. Here’s how personalized service can benefit you:

- Dedicated Attention: With a smaller client base, loan officers at smaller lenders can devote more time to each borrower. This means that you’re likely to receive more detailed advice and answers to your questions throughout the mortgage process.

- Tailored Solutions: Often have the flexibility to customize mortgage solutions based on your unique financial situation.

- This can be particularly beneficial if you have specific needs or if your financial situation is non-traditional.

- Streamlined Communication: Direct access to decision-makers can make communication more efficient.

- You’re less likely to be passed around from department to department.

- You can build a relationship with a single point of contact who understands your entire mortgage journey.

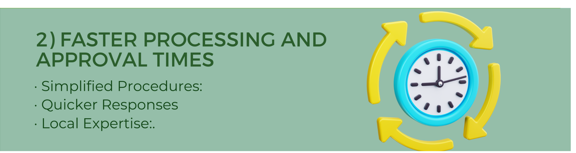

2. Faster Processing and Approval Times

Smaller mortgage lenders often have more streamlined processes and fewer bureaucratic hurdles compared to large banks. This can result in faster processing and approval times:

- Simplified Procedures: Smaller lenders may have less red tape and more straightforward procedures, allowing for quicker decision-making.

- This can be particularly advantageous if you’re in a competitive housing market and need to secure financing quickly.

- Quicker Responses: With fewer layers of management and a smaller team, smaller lenders can often make faster decisions on loan applications and respond more quickly to any issues that arise.

- Local Expertise: Smaller lenders are often deeply embedded in their local markets.

- Their understanding of local real estate trends and property values can contribute to faster and more accurate processing of your mortgage application.

3. More Competitive Rates and Terms

Despite the common perception that large banks always offer the best rates, smaller lenders can often provide competitive or even better rates and terms. Here’s why:

- Lower Overhead Costs: Smaller mortgage companies typically have lower operating costs compared to large banks. They don’t need to maintain extensive branch networks or employ large teams, which can reduce their expenses.

- These savings can be passed on to borrowers in the form of better rates.

Flexible Pricing: may offer more flexible pricing structures and be willing to negotiate rates and terms based on your specific financial situation.

- This can result in more favorable loan conditions.

- Customized Products: Often offer niche products or customized loan options that aren’t available with larger institutions.

- This can include specialized loans for first-time homebuyers, veterans, or those looking to invest in non-traditional properties.

4. Greater Flexibility in Underwriting

Flexibility in underwriting is another significant advantage of choosing a smaller lender. Here’s how smaller lenders can offer more flexibility:

- Less Rigid Criteria: Smaller mortgage companies may have more relaxed underwriting criteria compared to larger banks.

- This can be particularly beneficial if you have a unique financial situation.

- Such as a non-traditional income source or a less-than-perfect credit score.

Personalized Evaluation: Smaller lenders are more likely to review your application holistically rather than relying solely on automated systems.

- This means they may take the time to understand your entire financial picture, which can lead to more favorable loan terms.

- Creative Solutions: In cases where traditional underwriting criteria may not fit.

- Smaller lenders might be more willing to explore creative solutions or offer alternative loan products that better suit your needs.

5. Smaller Mortgage Lenders and community Focused, Local Knowledge

Smaller companies often have a strong community focus and deep local knowledge, which can be a significant advantage:

- Understanding of Local Markets: They are typically more familiar with local real estate markets, including neighborhood trends, property values, and zoning regulations.

- This expertise can help them provide more accurate and relevant advice for your mortgage needs.

- Community Relationships: Smaller lenders often build strong relationships within their communities, including with real estate agents, appraisers, and other local professionals.

- These relationships can facilitate a smoother mortgage process and help you connect with trusted resources.

Investment in Local Economy: By choosing a smaller, local lender. You’re supporting businesses that are invested in the economic growth of your community.

- This can have a positive impact on local job creation and economic development.

6. Enhanced Transparency and Trust

Trust and transparency are crucial when navigating the mortgage process. Smaller lenders often excel in these areas:

- Clear Communication: Smaller lenders are generally more transparent about their processes, fees, and terms.

- You’re less likely to encounter hidden fees or confusing terms. Any questions or concerns are more likely to be addressed promptly.

- Personal Relationships: Building a personal relationship with your lender can enhance trust and confidence.

- With smaller lenders, you’re more likely to interact with individuals who are genuinely invested in helping you achieve your homeownership goals.

- Reputation for Service: Smaller lenders often rely heavily on their reputation within the community.

- As a result, they may prioritize customer satisfaction and go the extra mile to ensure a positive experience.

7. Support for Non-Traditional Borrowers

If you’re a non-traditional borrower, such as a self-employed individual or someone with a unique financial situation, smaller lenders can offer significant advantages:

- Flexible Documentation: Smaller lenders might be more open to alternative forms of documentation and less stringent requirements for income verification compared to large banks.

- Customized Solutions: They can offer specialized loan products tailored to the needs of non-traditional borrowers, such as self-employed individuals or those with irregular income streams.

- Understanding of Unique Situations: Smaller lenders often have experience working with borrowers in non-traditional situations and can provide more personalized guidance to help you secure a mortgage.

8. Local Decision-Making

In some of the smaller lending companies, you will find that the decisions are often made locally. Which can offer several benefits:

- Localized Understanding: Local decision-makers have a better understanding of the regional market and can make more informed decisions based on local conditions.

Faster Decision-Making: Local decision-making can speed up the approval process, as decisions are not subject to lengthy review processes from distant corporate offices.

Flexibility in Approach: Smaller lenders may have more leeway to adjust their approach based on local market conditions and the specific needs of borrowers.

9. Smaller Mortgage Lenders can provide better Client Relationships and Support

Smaller lenders often pride themselves on building strong relationships with their clients, which can translate into several advantages:

- Long-Term Support: Smaller lenders are more likely to offer ongoing support. They are very focused on maintaining relationships with their clients, even after the mortgage has been closed.

- This can be valuable for future financial needs or questions.

- Client-Centric Approach: A client-centric approach means that smaller lenders are more focused on providing a positive experience. Throughout the mortgage process they will be very transparent and personally will talk to the client in some cases

- Community Engagement: Smaller lenders are often more involved in community activities and events, which can strengthen their connection to local borrowers and provide additional support and resources.

Conclusion

Choosing a smaller mortgage lender can offer a range of benefits, from personalized customer service and faster processing times to competitive rates and local expertise.

Smaller lenders often provide a more flexible, transparent, and community-focused approach, making them a compelling option for many homebuyers.

So, whether you’re a first-time buyer, a seasoned investor, or someone with a unique financial situation, considering a smaller mortgage company can lead to a more tailored and positive mortgage experience.

As you embark on your homebuying journey, exploring the advantages of smaller lenders can help you find the right mortgage solution for your needs.